Blog Post

The Current State of Core Insurance Technology Part 4: The Operating Environment

In this series, we share insights from a recent study* which seeks to understand the current state of core insurance systems and market sentiment for adopting SaaS-based models.

While diving into the priorities of insurance organizations, it’s essential to look at the technical environment in which these priorities will ultimately be executed. Insurance policy, billing, and claims solutions run on platforms ranging from private or public cloud platforms to on-premises systems or a hybrid derivative. Organizations need to ask themselves, is their platform capable of supporting the business’s innovation and growth initiatives?

As insurers depend on their core systems to effectively run and manage their business, ensuring the right fit between platform and business priorities is key. One important consideration is cost.

As core solutions age, the need to update them to account for technological advances increases. For example, on-premises systems require extensive and costly end-to-end support from the insurer organization for ongoing development and maintenance. On the other end of the spectrum, multi-tenant SaaS vendor platforms improve the bottom line by sharing hardware, software, and cloud computing costs among hosted tenants.

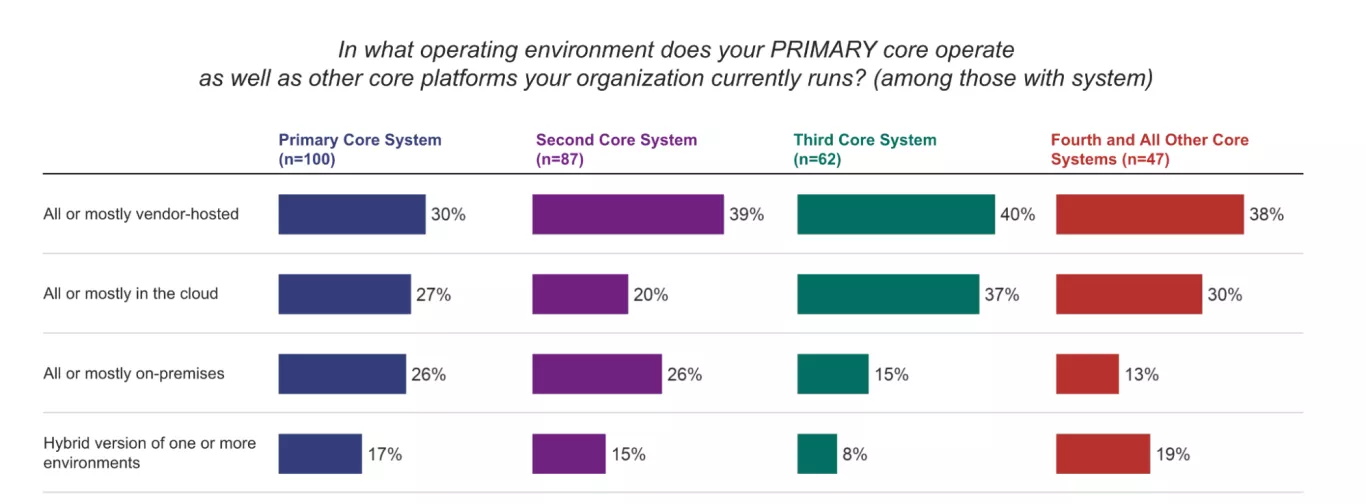

Surveying primary core systems, we found the average lifetime for a core platform to be 7.7 years with 31% less than 5 years old and 15% being employed for at least 10 years. Hybrid models represented the smallest share of extant environments, followed by on-premises, although the data did not correlate environment selection with overall direct written premium and associated market share. Vendor-hosted environments, common for SaaS applications, were most frequently used without respect to the number of core systems employed.

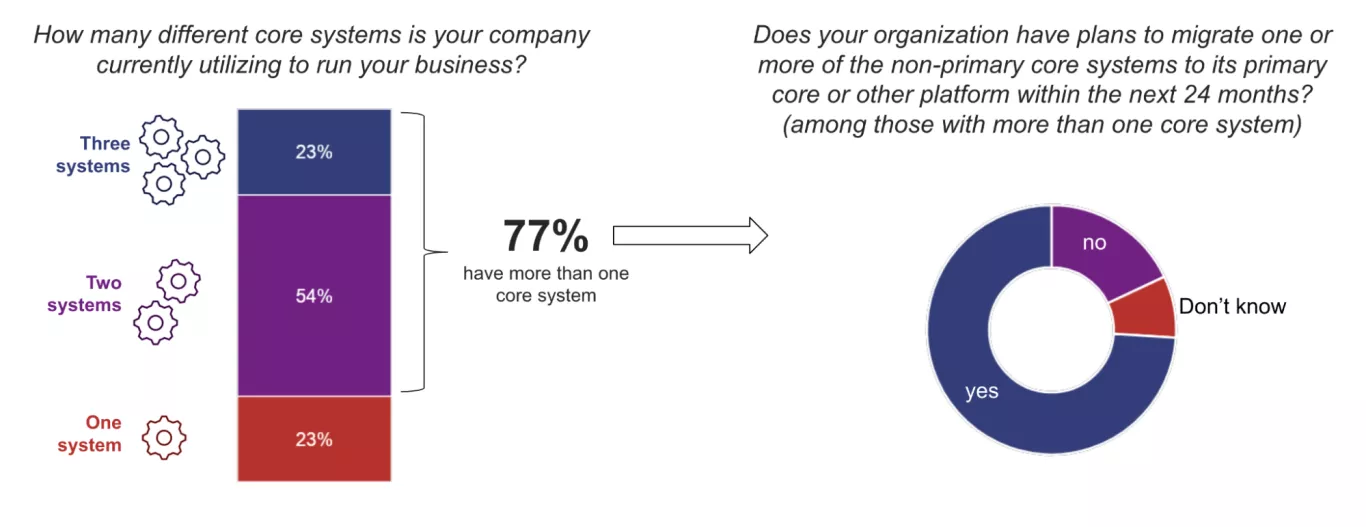

Most insurers (77%) in our survey utilize more than one core system and there’s little consistency in the vendors or the operating environments they’ve selected. Of those insurers using two or more systems, nearly three out of four have plans to migrate systems within the next two years. Every respondent with on-premises systems had plans to modernize in the next 10 years or more while 50% with private cloud systems planned to do so within the next 6-10 years.

Another objective of the study was to understand to what degree insurers felt their core systems helped them differentiate in the market. In 2019, IBM’s “Insurance on the Platform” research took a look at the degree to which bespoke legacy systems actually contributed to a competitive advantage.

“Insurers still remain tied to their traditional ways of working. They view legacy IT systems as a central part of their business model. Seventy-six percent of our survey respondents cite back-end systems as part of their organization’s core competency. Additionally, 75 percent of respondents view their back-end systems as a differentiating factor.

“If this were true – that is, if insurance systems really were a differentiator – they should generate a measurable and positive impact on business outcomes. For legacy systems to confer a competitive advantage, however, the differentiator would not be the systems themselves, but rather what the insurer could do with them: build innovative products to distinguish the organization in old or new markets, lower time-to-market, or produce better and faster service. Achieving these results requires built-in system flexibility. So all other things being equal, we expect insurers with newer systems would actually be more successful; similarly, insurers with fewer systems and insurers that have to spend less to maintain their systems would likely be more successful.”

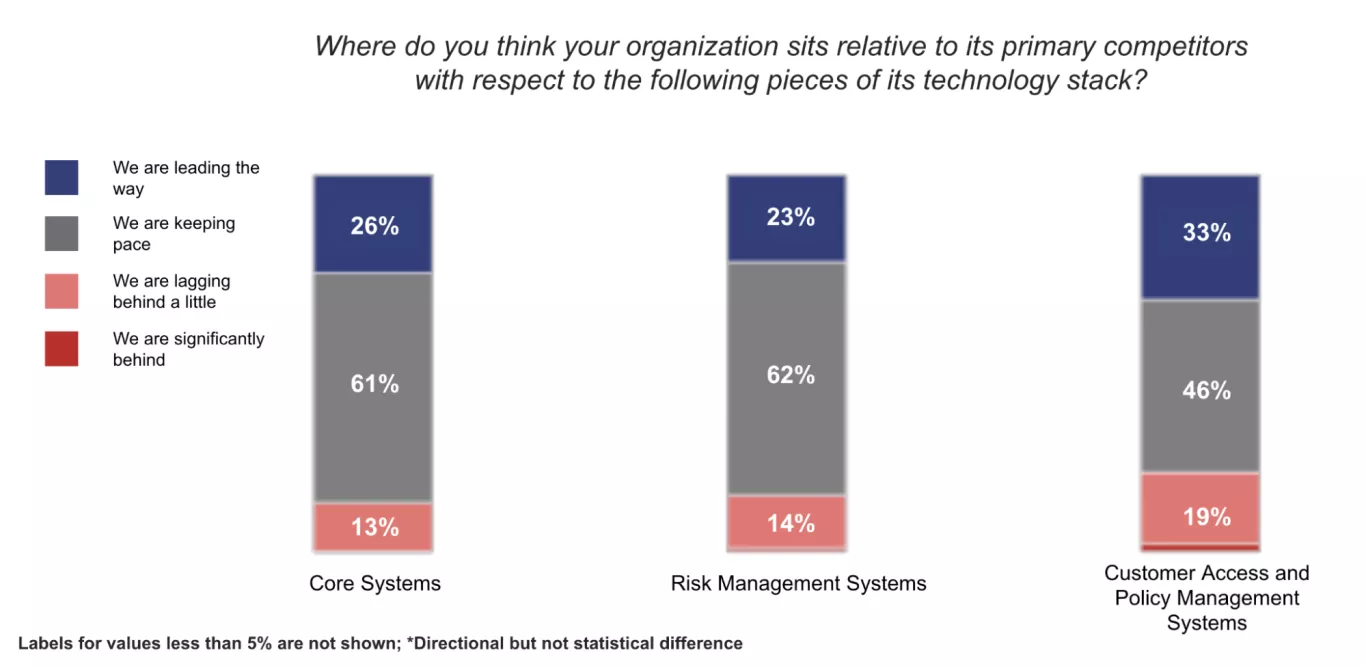

To understand the evolution of this perspective, we asked how organizations viewed core technology stacks against those of their competitors. Our survey revealed that while most don’t feel their systems are necessarily lagging behind others, they don’t feel they are leading the way either. This is particularly interesting when you consider that in part 1 of this series, we learned that 45% of respondents felt their legacy technology stacks impeded their progress toward key organizational priorities which in many cases were meant to differentiate them in the marketplace.

Delving deeper, insurance carriers had a higher percentage of respondents (46%) with opinions reflecting they are leading the way for P&C core systems. That number jumps to 54% for respondents with all or mostly on-premises systems, further confirming that insurers often still feel that on-premises environments provide a competitive advantage.

While outstanding questions remain regarding the specific competitive advantages insurers feel their systems provide, our study illustrates a strong correlation between core technology and the feasibility to execute on strategic priorities enabled by those platforms. Additionally, regardless of the system itself, the general inclination is to modernize core platforms more frequently than perhaps has been done in past years, taking advantage of technological advances and the capabilities they provide.

To learn more about why the architecture matters for selecting core insurance cloud technology, download our eBook.

*Research Methodology and Respondent Profile

This research was commissioned by Origami Risk and conducted by Arizent/Digital Insurance between September 22 and October 20, 2022, among 100 qualified respondents. To qualify, insurance industry professionals had to have a management role (in a non-legal/HR function) and have knowledge of their organization’s core systems or primary supporting services.

51% of respondents self-identified as P&C insurance carriers, 25% insurance broker/agent, 12% MGA/MGU and 12% third-party administrators.

Total Respondents: n=100; Annual premiums under $1B: n=35/Annual premiums of $1B or more: n=65; IT/technology role: n=16; Primary core system is all or mostly on-premises: n=26; Senior business unit executive: n=28/Division or dept head/director: n=36.